The Goods and Services Tax has alleviated the method of indirect taxation significantly since its introduction in India in 2017. However, despite the relative simplification with regard to the previous tax regime, it’s still within the emergent stages. There’s still some extent of fuzziness regarding its functioning among the profession in India. A business, in due course of its operations, needs to contend with an array of GST forms to accommodate its several tips and guarantee they reap its full advantages. One in every of these is that the GSTR 2A type. Understanding what it’s, its significance, and the way it fits within the GST system is, thus, imperative. We have our specialized GST consultants in Chennai to simplify the process even better.

What is GSTR-2A?

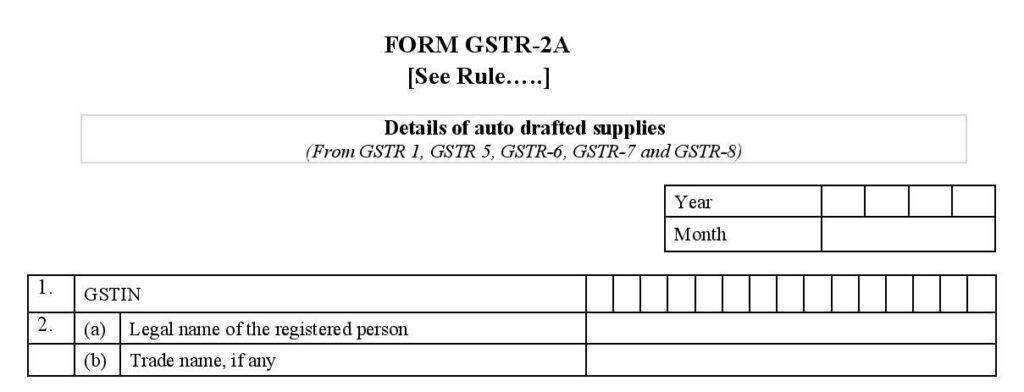

The GSTR-2A is related to purchase legal instrument that’s mechanically generated for every business by the GSTN portal. It’s supported the data contained within the GSTR-1, GSTR-5, GSTR-6, GSTR-7 and GSTR-8 of your suppliers. You’ll verify and amend this come back before you file it within the GSTN portal as your GSTR-2. GSTR 2A could be a purchase-related income tax return that’s mechanically generated for every business by the GST portal. Once a merchandiser files his GSTR-1, the data is captured in GSTR 2A. It takes info of products and/or services that are purchased during a given month from the seller’s GSTR-1.6

Filing process of GSTR-2A

Since it’s a read-only document that’s auto-populated supported alternative forms, a business doesn’t have to be compelled to file it. However, businesses have to be compelled to settle for it, reject it, modify it, or defer its acceptance if such associate degree organization finds any discrepancy within the invoice details that its vendor submitted in GSTR one.

Also, since it’s generated mechanically, there’s no GSTR 2A day of the month in question. However, if any info in this kind needs modification, businesses shall do thus in GSTR a pair of and also the day of the month for that’s between eleventh and fifteenth of a month straight away following the month that such GST come is filed.

Briefing on GSTR-2A-Part-A

- GSTIN: Goods and Services Taxpayer Identification Number (GSTIN) your unique PAN-based 15-digit number.

- Name of the Taxpayer: You need enter the legal name of the registered person and if any trade/business name can be included.

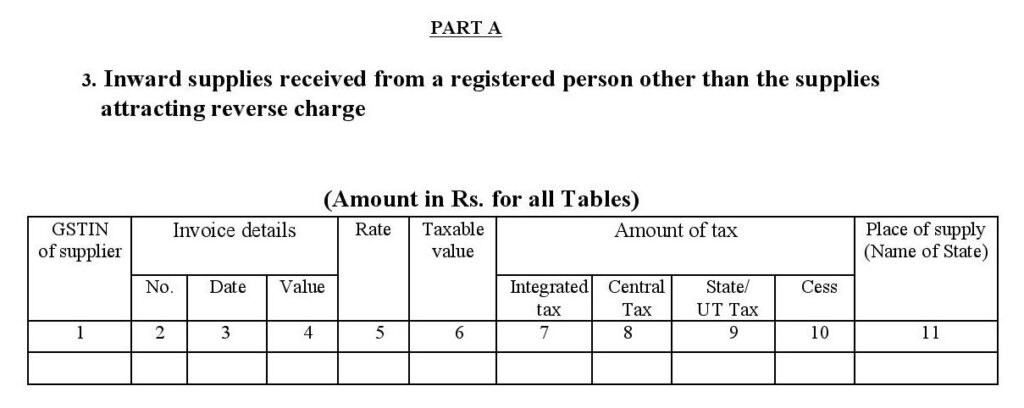

- Inward Supplies from Registered Taxable Person other than the supplies attracting reverse charge: Invoice-wise details of all purchases and provides received from alternative registered taxpayers, excluding those who might attract liabilities below a reverse charge basis.

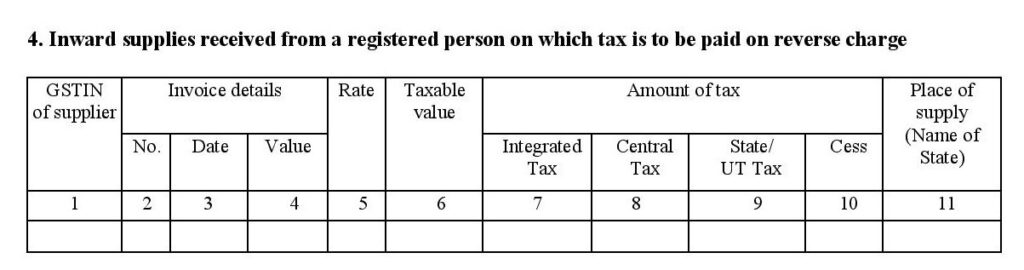

- Inward supplies on which tax is to be paid on reverse charge: All purchases and provides received (from each dutiable and non-taxable persons) that the client has got to pay taxes underneath reverse charge.

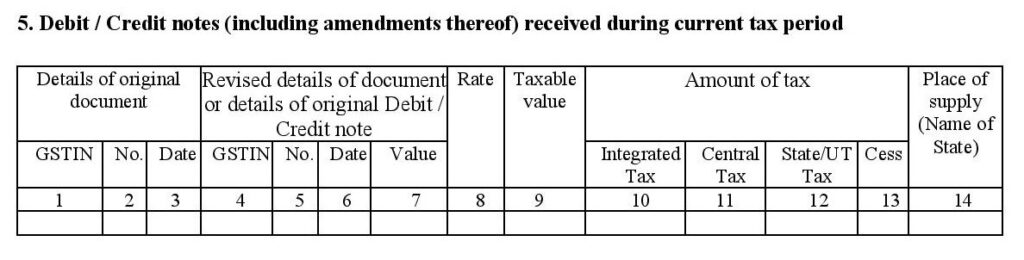

- Debit / Credit notes (including amendments thereof) received during the current tax period: Captures the small print of debit notes and credit notes issued by your vendors for this month in conjunction with any changes created to them by comparison the revised documents with the first documents.

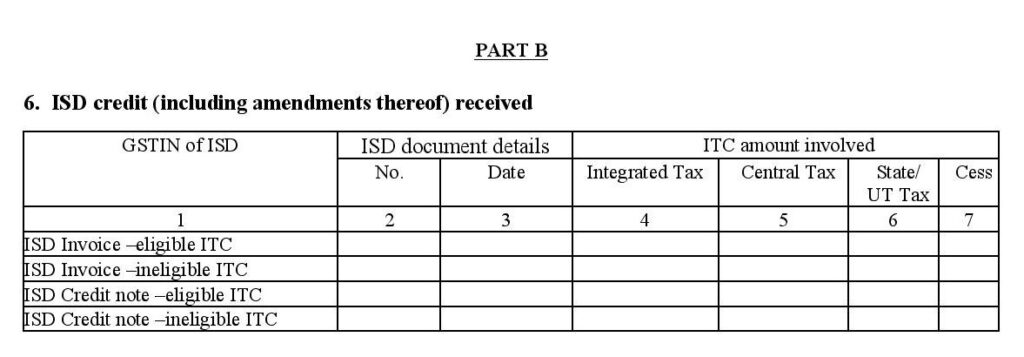

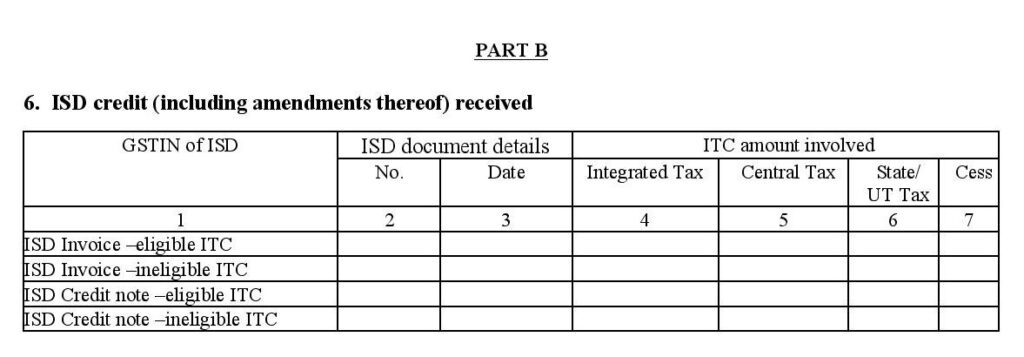

Briefing in Part-B

ISD credit (including amendments thereof) received: If your firm is an input service distributor, then the information underneath this section are going to be auto-populated whenever your head workplace files the GSTR-6 come for a selected month.

Briefing in Part-C

TDS and TCS Credit received (including amendments thereof): If you interact in TDS (tax subtracted at source) transactions, or sell on-line through AN e-commerce operator, this section are auto-populated from the transacting party’s GSTR-7 or e-commerce operator’s GSTR-8. As an auto-generated document, it can’t be filed directly into the GSTN while not the taxpayer’s intervention, therefore it doesn’t have a declaration at the top of the document.

Latest 38th GST meeting update

If the input step-down claims associated with associate invoice or a debit note isn’t mirrored in FORM GSTR2A, then the number of ITC claim are going to be restricted to 100 percent (earlier 20%) of the eligible credit offered to the business owner.

Difference between GSTR-2A and GSTR-2

- GSTR 2A is Associate in auto-generated browse solely document for info functions solely. Whereas GSTR-2 is a political candidate come back that’s to be filed Info in each the returns ar an equivalent.

- GSTR two may be altered, whereas GSTR 2A can’t be altered

Feel free to contact the GST consultant in Chennai for a more relaxed effort.

{kind=link}